Payroll Journal Entry for QuickBooks Online

In this article we will provide an example of how you can enter your payroll transactions into your QuickBooks Online account for the proper recording of wages, employer tax expense, net checks, and associated transactions related to payrolls being generated outside of the QuickBooks payroll application. If you are a subscriber to one of ASAP's accounting packages, this entry is likely already being performed.

In this article

Option 1: Journal Entry as a Recurring Transaction

Step 1: Set up a Journal Entry in QBO as a Recurring Transaction:

- click on the Settings Menu in the top right corner of your QBO account

- Select Recurring Transactions

- Select "NEW" from the upper right-hand corner of screen

- Select 'Journal Entry' as the Transaction Type, hit OK

- Give the template a name such as "Payroll". The Type should be "Unscheduled"

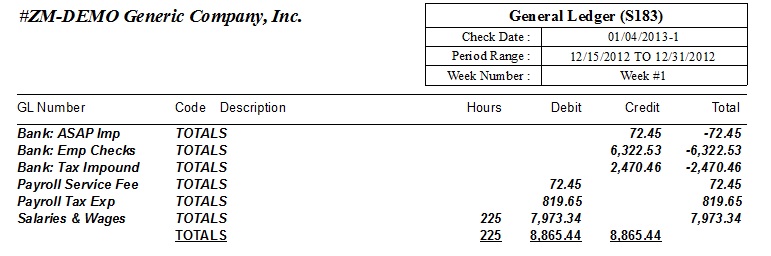

Step 2: Use the Journal Entry Template you named "Payroll" and reference your payroll reports. Below is an example using ASAP's General Ledger (S183) Report.

- Adjust the Journal Number; enter either check date or pay period end date as the entry date depending on your accounting method

- Update the amounts to match the GL Report provided in your reports file.

- Double-check to ensure it balances and hit Save to post the transaction.

Return to top of page

Option 2: Custom Import File or API Sync

An API sync between ASAP's core payroll suite and QuickBooks Online is in development. For the time being, we recommend setting up an import which is reliant on a third-party app to convert the files & post to QuickBooks Online. Keep in mind, if you are a subscribers to one of ASAP's accounting packages your payroll journal entry is likely already included.

A few quick points related to payroll journal entries:Net vs. Gross Payroll - Gross payroll is the total amount you pay your employees (Salary or Rate x hours) BEFORE taxes or other deductions. Net payroll is what your employees receive AFTER taxes & deductions. Employer tax expenses are based on the Gross Pay + Employer Taxes not the net checks or employee tax withholding. Often new employers confuse how their expenses (Debits in the journal entry) differ from the cash side transactions posting against their bank accounts (Credits in the journal entry). If an employee elects to take out more Federal or State withholding taxes, this has no impact on your over all payroll expense, but does increase the tax amount being impounded from your account. Conversely, should an employee elect to take out more taxes, it would reduce the net amount of each employee's check posting against your bank account. Thus don't get too hung up on the amount of the bank transactions on the credit side, it is more important to study the debit side expense lines.Accounting Method; cash basis or accrual basis-if you are not a subscriber to one of ASAP's accounting packages; it is best to consult with your CPA on how your books should be structured. This would impact how you should date each payroll transaction; by pay period end date or check date. For example, if you use the accrual method of accounting you would date your payroll entries by pay period end date. Whereas if you use the cash method you would date your payroll entries by check date as the expenses do not occur until they have been issued.